The problem is pretty evident. These are the most recent complaints I've been sent / forwarded in the last couple of weeks.

Anon Morpho Borrower Would you be able to ask {anon1} to stop doing whatever it is they are doing in this market? They are continuously depositing and withdrawing and spiking the rates over and over. We would like to be a much larger borrower in the market, but cannot due it with whatever they are doing, and going to have to unwind at this point.

**Anon Morpho Collateral Issuer **These {anon1} motherfckers are continually fcking with my market by depositing and withdrawing. I just got {anon3} to add more assets and they just withdrew to keep it just above 91.5%. Fck these guys, everyone is so pssed with them.

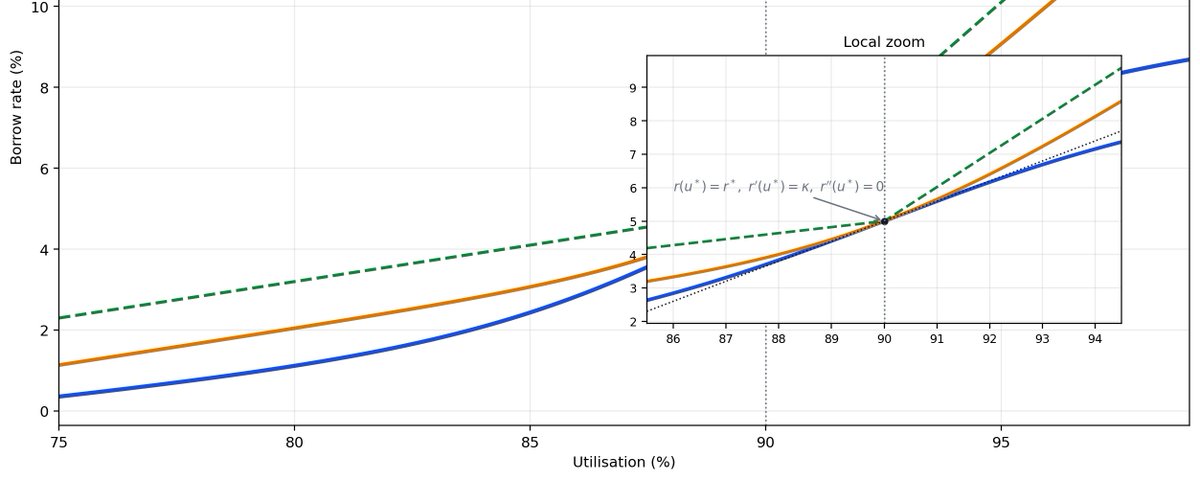

Most DeFi lending protocols use an interest rate curve with a kink in it. That means the borrowing rate rises one way up to a target utilisation, then suddenly becomes much steeper after that point.

This is simple and intuitive. But it also creates a problem: incentives change too abruptly at exactly the point where the protocol is trying to guide behaviour.

The job of an interest rate model is not just to set a number. Its real job is to shape behaviour around a target utilisation. Good design means the curve should guide the market smoothly back toward the target. Bad design means the curve creates a cliff-edge change in incentives right at the target.

That is the main weakness of the standard hard kink.

Why the hard kink is a weak design

The hard kink is easy to understand:

below the target, rates rise at one slope

above the target, rates rise at a steeper slope

But the transition is too sharp.

At the target, the slope of the curve jumps suddenly. In plain English, that means the protocol is trying to steer the market with an incentive cliff rather than a smooth steering wheel.

That is why the hard kink is better thought of as a rough reference point than as the best curve to run in production.

The two smoother alternatives

(1) The soft kink

The soft kink keeps the spirit of the hard kink, but smooths out the corner.

Once utilisation gets too high, it can shut off borrower incentives more sharply than a broad smooth curve.

But there is a cost. That sharper shutoff also makes borrower returns bend more sharply around the target.

That matters because sharper bending can make borrower outcomes more fragile when utilisation moves around.

(2) The twisted logistic

The twisted logistic is designed around the target itself.

The point is not just that it is smooth. The point is that it gives a clean local shape around the operating point:

the right target rate

the right local sensitivity

no awkward one-sided bend at the target

That makes it a good benchmark for asking what the other curves are adding or taking away.

Why this matters economically

There are two groups that matter in a lending market:

lenders

borrowers

When utilisation moves away from the target, the protocol wants the correct group to respond. In some markets, the important response comes from lenders reallocating capital. In others, especially faster-moving crypto markets, the borrower side reacts more quickly.

A more severe borrower penalty does not automatically mean better borrower behaviour. If the curve also makes borrower returns riskier, risk-adjusted demand can get worse rather than better.

So the real question is not

Which curve punishes borrowers more?

The real question is

Which curve creates the best risk-adjusted incentives around the target?

The trade-off

The soft kink and the twisted logistic each solve a different problem. The soft kink is better if you want a more forceful shutoff once utilisation gets too high.

The twisted logistic is better if you want a cleaner and more balanced local shape around the target.

That leads to the core trade-off:

the soft kink gives stronger local discipline above the target

the twisted logistic gives a cleaner and less fragile local incentive shape

Initial Conclusions

The hard linear kink is the weakest design because it creates a cliff-edge change in incentives.

The twisted logistic is the clean benchmark because it is built around the target in a disciplined way.

The soft kink can be useful, but its sharper shutoff comes with a cost: it can make borrower outcomes locally riskier than under the twisted logistic.

So the best design question is not whether a curve is smooth in some general sense. It is whether the curve creates the right behaviour around the target without introducing unnecessary fragility.

Next Steps

The trade off with targeting zero curvature at the target rate is a higher gradient. This practically translates to more interest rate sensitivity for the borrower position. Given the aims of stabilising the borrower positions, this seems like a sub-optimal situation.

As a result, we will look at whether the twisted logistic has additional value to add over and above the soft-kink when we stop targeting a zero second order derivative. Visually that means it would look a lot more like the soft-kink as can be seen in Figure 5.

The analysis we're looking at right now involves looking at the risk profile of a borrower's PnL to determine whether the negative curvature (shown in the bottom plot with the blue lines dipping below zero) has meaningful positive impact on the borrower PnL risk profile.