It’s impossible not to notice and it has already been broadly discussed that onchain yield has compressed everywhere: borrowing rates are converging with Fed rates and “safe” supply rates are averaging ~3%, which is below treasuries, SOFR, etc. etc. Most notably, at the time of writing the yield (30d average) on USDC and USDT on Aave is around 2%, Steakhouse and Gauntlet Prime offer ~3.2% (though yields are more competitive on Base), sUSDe provides 3.5%. Out of more than $20b in vaults on Ethereum and L2s, 58% of stablecoin TVL is earning under 3% APY, and 35% earn 3-5% APY. This has made the 4-3.75% yield from @SkyEcosystem USDS Savings an appealing refuge. But how can they offer a higher‑than‑average rate while having one of the biggest TVLs?

Of course, a direct comparison of Sky’s savings rate with Aave or Morpho lending rates is not entirely accurate, since the latter are purely derived from borrowing demand and utilization, while in the former (i) governance sets its rate (stability fee/SSR) and (ii) Sky can lend against whatever collateral Sky wants, including offchain origination (though the double‑edged sword of this approach is a less flexible and higher borrowing rates in its ecosystem).

However, all these projects do compete on the supply side, and considering that Sky acts as a central bank with exposure to most yield sources via uncollateralized credit lines to different entities it makes an interesting exercise to explore – what the nature of those yield sources is, what the ratio is between onchain and real‑world sources, and how correlated and scalable they are?

As @RuneKek himself was saying “over $300B worth of stablecoins are currently not earning any yield”... but how much of such potential demand might be accommodated?

Onchain yield map

To start tackling this loaded question and before diving into Sky’s balance sheet and financials, let’s take a brief detour to explore how yield on a chain is generated and what the numbers looked like in 2025.

Borrow interest

As in traditional finance, money markets are at the heart of DeFi too, accounting for more than 60 % of total DeFi TVL and generating roughly $1.76 billion of borrow interest (including CDPs and un/under-collateralized lending) in 2025. But what's the motivation to borrow? Since there are three established lending models (monolithic liquidity pools such as Aave v3, isolated pools with risk curators such as Morpho, and a central‑bank model with Sky and its stars), let’s examine each of them.

There are essentially three core groups of activities that drive borrowing:

Recursive lending. One use case is maximizing the yield of a yield‑bearing asset by borrowing its correlated equivalent and looping it. On Aave Ethereum v3 today, about 39% of borrowing demand is to leverage ETH staking rewards, which is consistent with even higher (45%+) historical performance with Fluid, Etherfi and Lido being the main counterparties. Borrowing demand for sUSDe looping is roughly 11.6 %. On Morpho, at least 27 % of borrowings participate in USD looping strategies directly within the protocol, farming sUSDS, syrupUSDC, sUSDe and similar assets; about 5% are in ETH strategies.

Now here we can see an advantage of adding markets dynamically – it helps avoid missing key “safe” yields (as we’ll later learn), especially in this economy.

2. Carry trades and leverage. The next subset of use cases (around 45 % on Aave) involves borrowing stablecoins against non‑stable assets (BTC, ETH etc(not ETC).) to make them capital‑efficient by supplying them elsewhere earning a spread. For instance, the top borrower on Morpho (6.5 %) takes USDC and deposits it into Sky Savings. Another big use case is going spot‑leveraged long (what top borrowers 0x54d25/xed0c6, 0x28a55, 0x741aa on Aave are exactly doing) or acquiring stablecoins for other reasons while keeping exposure to collateral. Today on Morpho, around 40% of interest is generated from loans against cbBTC (excluding the top borrower), with a big portion coming from Coinbase users.

3. Other minor motivations include borrowing non‑stable assets against stables** to short, or expressing any other pair thesis**.

As we can see, roughly half of the borrowing volume is about levering up another yield source, so two natural questions arise: Where is their interest coming from? When current strategies are exhausted, what other alternatives exist?

Network staking rewards

Yield from staking a native blockchain’s asset comes in two forms: network issuance and MEV rewards (priority fees plus bribes).

On Ethereum most of the staking yield comes from network inflation, with a relatively stable daily max issuance of about 2.7 k ETH, totaling around one million ETH in 2025; on Solana, issuance was roughly 24-25 million SOL. A strong side of this sub‑source is that it is consistent, though the principal is volatile.

Around 5-20 % (5-30 % on Solana) of staking rewards come from and depend on onchain activity (priority fees and MEV) and this portion has been trending down since the Merge. Why? Roughly half of MEV comes from arbitrage and half from frontrunning. The latter has decreased because of MEV-resistant tools such as OFAs and solvers (now about 90 % of swaps are routed privately), while the former used to be internalized mainly by non‑neutral searcher‑builders and is now very market‑dependent and competitive.

Funding rate

Funneling perps funding fees onchain was a great deal brought by Ethena which generated ~240m in fees (~90% coming from funding) in 2025, totalling ~$300m in this category. This instrument is particularly interesting because:

It introduced a new source of yield to DeFi in a tokenized and composable manner

It’s relatively easy to capture

It’s persistent meaning it’s “always” there even though

it's market-dependent and volatile (for instance, in 2021 it returned 16%, in 2022 0.6%, in 2023 ~9%, and in 2024 returned ~13% APY)

which makes it a fitting underlying for derivatives like fixed‑interest rates and interest‑rate swaps (compared with LSTs or lending‑protocol APYs) as observable on Pendle.

While the question how scalable this source is a separate question, in 2025 BTC perps OI fluctuated between $35-65b, ETH perps OI was around $20-40b. Early 2026 shows total perps OI around $75b, with Ethena’s current share roughly 1.8%.

Trading fees

Swapping in any form has always been one of the top activities on blockchains (if not top 1), so selling shovels to take a cut from traders has always been an alluring endeavour. In 2025, AMM LPs made about $4.2 billion from trading fees, with 62% coming from Uniswap, Meteora, and Raydium.

However, capturing these fees in a structured product is not that simple:

LPs often lose money. Pools are exposed to toxic order flow, and a significant portion of LPs especially those providing concentrated liquidity end up losing capital (1, 2, 3 etc.), so this activity is typically left to sophisticated actors. Additionally, a mechanism to capture these fees in the form of Uniswap LP‑manager products has not gained much traction.

Limited composability. LP positions as collateral also have not got much traction

Concentration in short‑tail assets. A large share of trading fees comes from short‑tail assets that are unlikely to appeal to yield products. On Ethereum in 2025 roughly 25 % of volume came from ETH‑stablecoin pairs (now about 60 %), and 41 % from USD pairs. On Solana, 50 % came from SOL‑USD, memecoins accounted for 30 % and stablecoin pairs for 5 % (now the split is around 62‑12‑17 %).

AMMs vs PMMs. The scalability of AMMs is another debate. Even though most front‑end volume is routed through solver networks, only ~11 % goes through PMMs rather than AMMs. On Solana in 2025 proprietary AMMs had a 30 % market share; they now have about 60 % and dominate SOL‑USD pairs, consistently capturing more than 60 % of that market and peaking at 86 % on July 5.

Nevertheless, there are a few trading‑strategy vaults on Gauntlet, and the main guest of this article Sky has some exposure to AMM LPing as well (more on that later).

With DeFi perps gaining popularity, their MM vaults (HLP, LLP and others) can be viewed as alternatives to Uni LP managers. Returns to LPs have been modest (around $130 million) with JLP adding ~$670 million more. Naturally, risk curators are eying in this direction, and tl;dring a view from some of them about the risk profile of such products: “they [hlp, llp, giga vault, olp] have shown 5-9% drawdowns and multi-month underwater periods. Daily returns follow the market-making profile: many small positive days, a meaningful share of flat days, and occasional large losses. Yield can be excellent on a sharpe basis, but it is lumpy and path-dependent”.

Selling risk

There are three things one can do with risk: retain, mitigate and migrate (h/t @renatco). Today most participants primarily retain risk though they adopt advanced mitigation tools. Ways to offload (i) volatility or (ii) protocol risks (technical, economic, governance) are still very limited, so premiums from these directions are negligible, which might be an untapped opportunity.

Well, of course, decentralized options are not something new, and DeFi has seen a range of experiments, from options AMMs and perpetual options to some traction with DOVs, but unfortunately these vaults did not stand the test of time. A few teams continue to build in this sector, so hopefully we see more instances of captured tokenized volatility.

In terms of opportunity, CeFi options compete strongly with perps. Open interest varied between $30 billion and $50 billion in 2025, while current onchain OI is around $1.8 billion (mainly from Derive). Option premiums share similarity with funding fees in being persistent, but capturing and packaging them is a stretch assignment. As a speculative note, given that allocation space with risk curators has become more methodical and competitive, vaults might diversify into options to stay ahead.

Premium inflow from insurance underwriting remains very small, with most of it coming from veteran Nexus Mutual, on which over $5.5 million was generated for sellers in 2025 and which concentrates its exposure on Fasanara, Infinifi and Dialectic onchain products. With low current yields and the sheer nuances of pricing onchain risk, insurance is still young or perhaps DeFi is too young for it. As yield sources diversify and protocols’ lindiness increases, demand may finally grow. Other forms of insurance such as Aave’s Umbrella or more indirect mechanisms like topping up reserve funds from fees or a governance token can complement a specific protocol’s insolvency risk but are unlikely to fit into a structured product.

RWAs

As the purpose of this article is to explore onchain yield origination, RWA coverage will be limited to a rough approximation just to get a reference point and a glimpse of market overview. Consulting rwa[dot]xyz, we can see that total value grew from about $5.6b in 2025 to $27b today, with U.S. Treasuries holding the largest share at roughly 41 % and private credit at about 25 %. Resorting to primitive napkin math by applying a typical rate of return to the average value of each group throughout 2025 and adding yield‑bearing commodities and real estate – it can be estimated that these assets generated ~~~$600-900m of yield. The implications will be discussed later on.

Wrapping up this longer than expected detour, it is estimated that about $8 billion of onchain yield was genereted in 2025, but it's heterogeneous and some of it is not easy to catch even if you can (for instance, AMMs fees / volatility selling), and room for the safe yield is even smaller. However, with constant DeFi experiments and crypto-native opporunities (even if CeDeFi), we might see more onchain fees and mechamisms to capture them.

Sky

Let’s get back on track and see how Sky incorporates most of these yield sources into a coherent consistent strategy by analysing its 2025 performance and current positioning.

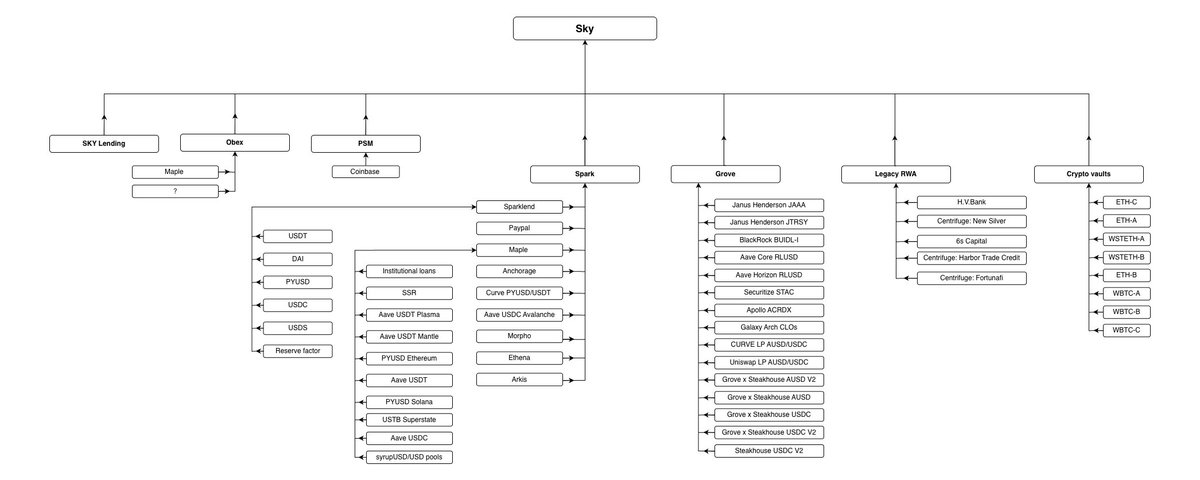

To start, today around 55 % of income comes from Sky’s own direct loans (PSM, crypto vaults, legacy RWA, lending against the SKY token) and 45 % from Sky’s stars to whom uncollateralized credit lines are opened.

The PSM remains the largest source contributing about 44% of income. In 2025, it provided roughly 27% of gross revenue which comes from USDC earning Coinbase rewards.

Crypto vaults now earn a roughly tithe-sized yield, with ETH and WSETH collateral bringing the most.

Direct exposure to legacy RWA (excluding the PSM) has been trending down. It is now obtained via the recently launched star @grovedotfinance whose cumulative revenue comes 47 % from Janus Henderson JAAA (cash‑like instruments and CLOs), 16.7 % from Janus Henderson JTRSY (treasury bills) and 15.2 % from BlackRock BUIDL‑I (cash‑like instruments).

@obexincubator is a newer credit line currently allocating all its resources (about $600 million) to syrupUSD, but it aims to be a* place d’armes* for yield‑bearing structured products.

@sparkdotfi's share of revenue and assets composition has been steadily growing since April 2025, overtaking the d3m credit line model and becoming the key allocation arm, producing 20-65 % of revenue. Spark acts as an asset manager and risk curator who (i) oversees its own lending protocol Sparklend (an Aave v3 fork), and (ii) allocates flexibly to yield‑generating opportunities (depending on whatever is lucrative these days within its risk framework) that exceed the borrowing cost (SSR plus 0.3 %). But where does the yield flowing into Spark come from?

Loans to Sparklend are the biggest asset on the SLL balance sheet making up 37 % (excluding distribution rewards) of total gross yield in February 2026 which is consistent with Q3 and Q4 (33.4% and 37.8% respectively). Why are onchain participants borrowing on Sparklend?

Since there is only one yield‑bearing token (WSETH) available as collateral, the first and major use case is a classic looping strategy. It accounts for around 50 % of borrowings, is a key contributor to reserve factor revenue, and is mainly executed by entities such as Ipor, Threehouse, Mellow and Summerfi.

Most of the rest is stablecoins borrowing. Only USDT’s interest model is decoupled from the SSR and based on utilisation, which may explain why it’s the second‑most borrowed asset (~25 %). Why would anyone borrow other stablecoins at a higher‑than‑average market rate? It’s not entirely clear. For instance, the top addresses borrowing on Spark are linked to 7 Siblings (0x3a0dc, 0x9cc65, 0x28a55), holding at least a 15 % share of total borrowed value (with a few hundred idle ETH supplied). Among their recent activities is levering ETH and SKY long → SKY staking, so keeping usage within the ecosystem plus revenue share and SPK farming could explain this. The next largest borrower is also continuously TWAPing into SKY → staking.

More than half of the revenue comes from allocations to other yield sources, and it depends on where the yield is now. For instance, in Q3-Q4 a significant chunk came from Morpho, Maple and Ethena (Q3), while today daily revenue comes from Maple (10.6 %), Anchorage (11.2 %) and PayPal rewards (30%).

So how does @maplefinance make yield? About 28 % of its liquidity is lent to institutional borrowers against blue‑chip collateral (BTC, XRP, SOL, HYPE) at 6-9 % APR, and the rest is deployed again to yield‑generating opportunities. A third of it goes back home to USDS savings, and the rest is deployed to Aave, PYUSD, Superstate and syrupUSD liquidity pools.

What about Anchorage? Institutional borrowing against BTC under 6.5 %

Morpho and Ethena? We’ve already seen their ins and outs.

Finishing up this brief overview of Sky’s financial affairs, it made $338 million and paid out $194 million to Savings in 2025. Today, the $6.7 billion USDS in Savings pays out 3.75 %, translating to ~$688 k per day in distributions while earning about $1.17 million. Based on current projected revenue composition snapshots, we see that the yield generated by Spark has a roughly 50 : 50 ratio between onchain and offchain origination, while Sky has a higher 70 % share of income coming from non‑onchain sources. What might that mean for all of us?

Regardless, where it’s being produced, there is a sustainable yield onchain that is much less dependent on market activity and leverage demand, and is not directly correlated with onchain sources, providing a sanctuary for capital to park for individuals and protocols. As for Sky, because of diversified and flexible allocation strategy, it can quickly adapt as risk appetite returns onchain. Additionally, as USDS becomes the largest yield‑bearing coin in real time and as we saw from the activity of some of the biggest borrowers, Sky indirectly can help a bit other protocols maintain rates on a par.

Some say that TradFi is eating DeFi and indeed many tokenized RWAs are permissioned with limited recourse to regular users. However, even though origination is happening offchain, the yield is funneled and re‑distributed onchain. This is important because it brings liquidity and a variety of yield to DeFi on which permissionless protocols can then capitalize. Moreover, it can help set off and scale the next layer of yield derivatives – fixed interest rates, interest‑rate swaps, risk tranches, and structured products – a real DeFi renaissance?